CWS: 3rd Quarter 2025 Portfolio Review

Market Review

The Fed had cut rates a few times in 2024, but until Q3, it had not cut rates in 2025. Gradually, Fed Chairman Jerome Powell and his colleagues at the Federal Open Market Committee grew convinced that the economy needed a shot in the arm.

Powell mentioned emerging weakness in the labor market. It’s not serious yet, but there are signs that the labor market is feeling stretched. The Fed also needs to deal with the tariff policy from the White House. This is especially difficult because we don’t know exactly what the policy or its implications will be.

Since April, the stock market has been remarkably calm and resilient. There were several events that could have easily knocked it into a nasty bear. In fact, we had a downturn in the early part of 2025. However, since early April, the stock market has been in a great mood. From the start of 2025 until April 8, the S&P 500 lost 15%. From April 8 until the end of Q3, the market gained 34%.

Not only have stocks been rallying, but they’ve been very stable. Consider that from the beginning of 2025 until June 16, the S&P 500 had 22 days where the index fell more than 0.8%, which isn’t that much. From June 16 to the end of Q3, the stock market has had a daily drop of more than 0.8% just once.

One of the important characteristics of the stock market during Q3 was the strong performance of risky stocks. By this, I mean large-cap technology stocks. On the other hand, smaller companies that were focused on more defensive areas of the market didn’t do very well. There’s been a growing gap in the market between risky stocks and conservative stocks. I can’t think of a recent time when the market has been so divided.

This could soon change. As the Federal Reserve lowers interest rates, more investors may come to favor conservative stocks. It’s always hard to pinpoint market rotations, but when they do come, they can be powerful.

In particular, three sectors of the stock market have not done very well in recent months. Those three sectors are utilities, consumer staples and healthcare.

Stocks in these sectors tend to have stable earnings and dividends. Investors often like these defensive sectors because the businesses are reliable. During the third quarter of 2025, however, they largely stayed away from these reliable areas of the market.

Investors became very willing to take on more risk in search of higher returns. This can happen for only so long, though. At some point the market will swing back and investors will return to defensive stocks.

Thanks to the federal shutdown in October, the government delayed its September jobs report. For August, the U.S. economy added 22,000 net new jobs. That’s not so hot. Wall Street had been expecting a gain of 75,000. The unemployment rate increased to 4.3% and is now at a four-year high.

The jobs number for July was revised higher by 6,000 to 79,000. The number for June was revised downward by 27,000 and now shows a jobs loss of 13,000. In July, it was originally reported as a gain of 147,000.

Average hourly earnings rose by 0.3%. That was in line with expectations. Over the last year, average hourly earnings were up 3.7%.

Hiring was held back by a payroll reduction in the federal government, which reported a decline of 15,000.

Healthcare again led sectors, adding 31,000 jobs, while social assistance contributed 16,000. Wholesale trade and manufacturing both saw declines of 12,000 on the month.

The manufacturing sector has shed jobs for the fourth month in a row. The broader U-6 rate increased to 8.1%. This was a weak report, and it gives more ammo to the interest-rate doves at the Fed. The U-6 (Unemployment) rate measures the percentage of the U.S. labor force that is unemployed, plus those who are underemployed, marginally attached to the workforce, and have given up looking for work.

Performance Review

Here’s how the fund did during Q3:

Source: StockCharts.com; from 04.01.2025 to 10.01.2025. Past performance is no guarantee of future returns.

Portfolio Review

Let’s look at some of the stocks that drove our performance during Q3.

Abbott Labs (ABT) was our first stock to report its Q2 earnings. For the quarter, Abbott made $1.26 per share, which beat Wall Street’s consensus by one penny per share. Management had told us to expect earnings between $1.23 and $1.27 per share. For the quarter, sales were up 7.4% to $11.14 billion. That beat estimates of $11.07 billion. If we only look at organic sales, then Q2 sales were up by 6.9%, and if we exclude Covid-related items, then sales were up 7.5%. For the first half of this year, organic sales were up 6.9% and non-Covid sales were up by 7.9%. For all of 2025, Abbott sees organic-sales growth rising by 7.5% to 8.0%. That’s slightly less than Abbott’s previous guidance for sales growth of 7.5% to 8.5%. Including Covid items, Abbott sees sales growth of 6.0% to 7.0%. For earnings, Abbott sees full-year profits ranging between $5.10 and $5.20 per share. That’s down from the company’s prior guidance of $5.15 to $5.25 per share. Abbott projects its full-year operating margin to be “approximately” 23.5% of sales. The prior guidance was for 23.5% to 24.0%. Last year, Abbott made $4.67 per share. That means that at the midpoint of this year’s guidance, Abbott expects double-digit earnings growth. For Q3, Abbott expected earnings ranging between $1.28 and $1.32 per share. Wall Street had been expecting $1.34 per share. The company is still doing quite well for us. Bear in mind that this is a stock that has increased its dividend for 53 consecutive years.

On July 22, Mueller Industries (MLI) reported Q2 earnings of $1.96 per share. That was up from $1.41 for last year’s Q2. I can’t say exactly if MLI beat earnings because only one analyst follows it, and he or she was expecting $1.62 per share. This was a good quarter for Mueller. Its net sales rose to $1.14 billion. At the end of the quarter, MLI had a cash balance, net of debt, of $1 billion. The CEO said he expects demand to increase once interest rates come down. I’m pleased with this report, and MLI continues to have a good valuation. This week the shares hit an eight-month high.

Amphenol (APH) had another outstanding quarter. For its fiscal Q2, the fiber-optic folks made 81 cents per share. That was above Wall Street’s forecast for 68 cents per share, and the company’s own guidance for 64 to 66 cents per share. Quarterly sales were up by 57%, and Amphenol’s operating margin reached 25.6%. During the second quarter, Amphenol bought back 2 million shares for $160 million and paid dividends of $200 million. For Q2, Amphenol expects sales between $5.4 and $5.5 billion. That represents growth of 34% to 36%. Amphenol sees earnings coming in between 77 and 79 cents per share, which reflects a growth rate of 54 to 58%.

Fiserv (FI) had a tough time this quarter. The numbers weren’t bad; the problem was guidance. For Q2, FI made $2.47 per share, which was up 16% from last year and a four-cent beat. Organic sales were up 8% to $5.5 billion. Fiserv’s operating margin increased 120 basis points to 39.6%. Free-cash flow was $1.54 billion in the first half of 2025, compared with $1.48 billion last year. The problem is that Fiserv lowered its outlook for organic-revenue growth from a range of 10% to 12% to “approximately” 10%. There was no change to the EPS outlook. The company sees 2025 earnings coming in between $10.10 and $10.30 per share. That’s growth of 15% to 17% over last year. This year is on track to be Fiserv’s 40th year in a row of double-digit earnings growth. The company also signed a strategic deal with TD Bank of Canada.

Moody’s (MCO) had another very good quarter. I feel like I say that a lot, but it’s true. For Q2, Moody’s made $3.56 per share. That beat the Street at $3.39 per share.

Moody’s business is really two businesses. There’s Moody’s Investor Service (MIS) and Moody’s Analytics (MA), which is the jewel in the crown. Last quarter, Moody’s companywide revenues increased by 4% to $1.9 billion. Revenues at MIS were flat at $1 billion, and revenues at MA increased by 11% to $888 million. For this year, Moody’s sees earnings ranging between $13.50 and $14.00 per share. That’s an increase to the low end by 25 cents per share.

Rollins (ROL) also had a good Q2. For the quarter, the bug people made 30 cents per share, which matched Wall Street’s consensus, and the stock rallied nicely on Thursday. Q2 revenues were up 12.1% to $1 billion, with organic revenues up by 7.3%. Rollins’s earnings rose 11.1% over last year. ROL’s operating-cash flow was up 20.7% to $175 million. The company invested $226 million in acquisitions and $7 million in capital expenditures and paid dividends of $79 million. The CEO said, “The demand environment is healthy, and we saw double-digit revenue growth across all major service lines.”

Thermo Fisher Scientific (TMO) did very well for us thanks to a solid earnings report. Over three days, TMO gained more than 17%. For Q2, Thermo made $5.36 per share. Wall Street had been expecting $5.23 per share. Q2 revenue grew 3% to $10.85 billion, and Thermo’s operating margin was 21.9%, compared with 22.3% for last year’s Q2. The results are encouraging, because TMO hasn’t done very well this year. Thermo also raised its guidance for sales and earnings. For this year, TMO sees revenues ranging between $43.6 and $44.2 billion, and earnings between $22.22 and $22.84 per share.

After the bell on July 24, McGrath RentCorp (MGRC) said it made $1.46 per share for Q2. The consensus on Wall Street had been for $1.22 per share. MGRC’s quarterly revenues were up 11% to $235.6 million. Sales revenues increased 28% to $69.8 million, and rental-operations revenues grew 5% to $163.5 million. McGrath also raised its outlook for this year. The company now sees full-year sales of $925 to $960 million. That’s an increase of $5 million to the low end. McGrath expects full-year EBITDA of $347 to $356 million. That’s up from the previous range of $343 to $355 million.

American Water Works (AWK) is the largest regulated water company in the United States. I’ll be honest: this is a dull stock, but that’s a reason to like it. After the close on July 30, American Water said it made $1.48 per share for its Q2. That was five cents below estimates. Despite the earnings miss, this wasn’t a bad quarter for American Water. In fact, the company raised the low end of its full-year range by five cents per share. AWK now expects 2025 earnings between $5.70 and $5.75 per share. The stock hasn’t done much recently. For the last several weeks, AWK has largely stayed within the low $140s. The shares currently yield about 2.4%. This is a very stable stock, and business is good.

FICO (FICO) had a great quarter, but Wall Street wasn’t impressed. For its Q3, FICO earned $8.57 per share. That’s up from $6.26 per share last year. It also beat expectations by more than 12%. This was a solid quarter. Revenue was up 20% to $536.4 million. FICO’s free-cash flow was $276.2 million, compared with $205.7 million last year. FICO also increased its full-year guidance from $28.58 to $29.15 per share. The company has already made $22.15 for its first three quarters, so that implies Q4 earnings of $7.00 per share. Despite the good results, the stock sank 6% in Thursday’s trading. What’s going on? The problem is that FICO has benefitted from recent price hikes. Interestingly, the company didn’t increase its revenue outlook for this year.

Intercontinental Exchange (ICE) reported Q2 revenue growth of 10% to $2.5 billion. Earnings were up 19% to $1.81 per share. That was a four-cent beat. ICE had an operating margin of 61%. This is such a strong company. Through Q2, operating-cash flow was $2.5 billion, and free-cash flow was $2.0 billion. This year, ICE bought back $496 million of stock and paid $555 million in dividends. The shares recently hit a new 52-week high.

After the closing bell on Thursday, Stryker (SYK) reported an 11.4% increase in quarterly earnings to $3.13 per share. The was six cents more than estimates. Net sales increased 11.1% to $6.0 billion, and organic net sales increased 10.2% Stryker has two major operating units. MedSurg and Neurotechnology had net sales of $3.8 billion. That’s an increase of 17.3%. Organic net sales increased 11.0%. That breaks down to 10.2% from increased unit volume and 0.8% from higher prices. Orthopaedics, the second operating unit, had net sales of $2.2 billion. That’s up 2.0%. Organic net sales increased 9.0% in the quarter, including 9.0% from increased unit volume. For the quarter, Stryker had an adjusted-operating-income margin of 25.7%. Now for the best news. Stryker is raising guidance. For this year, Stryker sees organic-sales growth of 9.5% to 10% and earnings between $13.40 and $13.60 per share.

Top Holdings

| Ticker | Security Description | Portfolio Weight % |

| IESC | IES HOLDINGS INC | 7.16% |

| APH | AMPHENOL CORP-CL A | 6.66% |

| COR | CENCORA INC | 5.26% |

| HEI | HEICO CORP | 5.11% |

| MLI | MUELLER INDUSTRIES INC | 4.82% |

| ROL | ROLLINS INC | 4.80% |

| ABT | ABBOTT LABORATORIES | 4.47% |

| ICE | INTERCONTINENTAL EXCHANGE IN | 4.30% |

| AWK | AMERICAN WATER WORKS CO INC | 4.26% |

| INTU | INTUIT INC | 4.07% |

As of 09.30.2025. Holdings subject to change.

Outlook

There are also several geopolitical risks. The world’s a dangerous place, and several flashpoints could cause mayhem for our markets.

I’d also point out that with gold soaring, there are more people concerned that our federal debt is not sustainable. Unfortunately, this is an issue that’s frequently ignored until it’s a problem. For now, it’s being ignored.

We should also be concerned with the state of the economy. Gains in the labor market have slowed to a crawl. We still want to see workers get higher wages. That’s good for them and good for our stocks. The inflation news has improved, but we’re still above the Federal Reserve’s target for inflation. I expect to see interest rates continue to come down this year and into 2026.

I’m forecasting a conservative and bullish environment for the rest of this year, but there will be weak areas. The housing market is a good example. Housing costs are too high, and I’d like to see them come down so new homes are more affordable.

I also expect to see a favorable earnings environment for Q4 and 2026. If any damage comes to the stock market, conservative stocks will fare much better. This is good news for the AdvisorShares Focused Equity ETF (CWS). I remain very optimistic for the stocks in our fund and our overall strategy. We beat the market during Q3, and I foresee these trends lasting for the rest of 2025 and into next year.

Eddy Elfenbein

Crossing Wall Street

AdvisorShares Focused Equity ETF (CWS) Portfolio Strategist

Management Fee

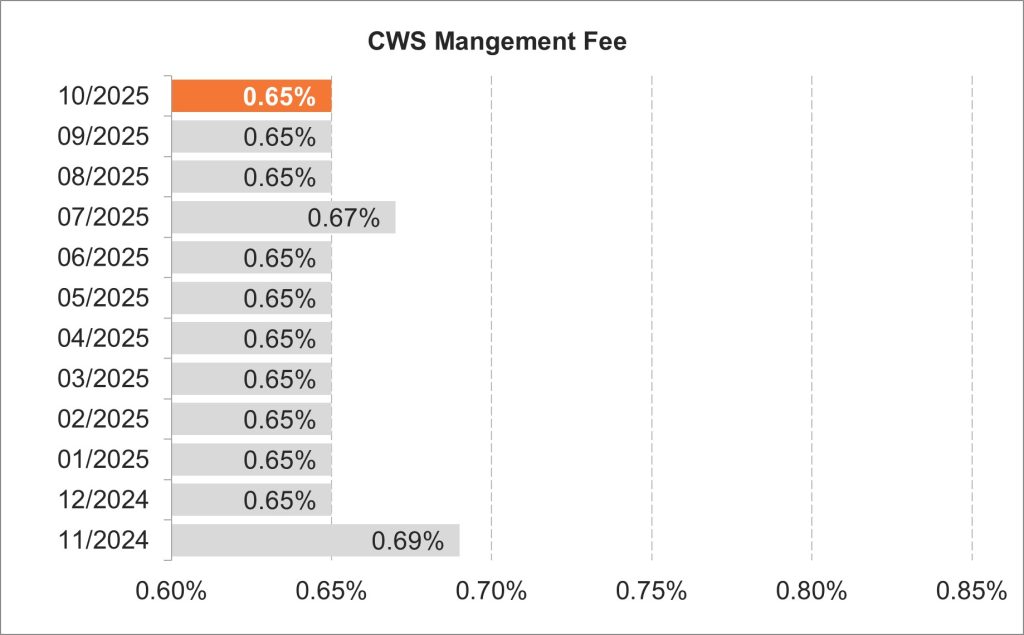

In a first for the ETF industry, the portfolio strategist of CWS has “skin in the game.” The strategist’s compensation is directly tied to portfolio’s performance. Using the trailing 12-month returns of CWS vs. its S&P 500 Index benchmark, stronger outperformance is rewarded with a larger management fee while weaker underperformance is penalized with a smaller management fee.

After the Fund’s September performance, the CWS fulcrum fee will be 0.65% in October 2025.

Past Commentary

A basis point is one hundredth of a percentage point (0.01%).

The S&P 500 Index is a broad-based, unmanaged measurement of changes in stock market conditions based on the average of 500 widely held common stocks. One cannot invest directly in an index.

Before investing you should carefully consider the Fund’s investment objectives, risks, charges and expenses. This and other information is in the prospectus or summary prospectus, a copy of which may be obtained by visiting www.advisorshares.com. Please read the prospectus carefully before you invest. Foreside Fund Services, LLC, distributor.

There is no guarantee that the Fund will achieve its investment objective. An investment in the Fund is subject to risk, including the possible loss of principal amount invested. The prices of equity securities rise and fall daily. These price movements may result from factors affecting individual issuers, industries or the stock market as a whole. Shares of the Fund may trade above or below their net asset value (“NAV”). The trading price of the Fund’s shares may deviate significantly from their NAV during periods of market volatility. There can be no assurance that an active trading market for the Fund’s shares will develop or be maintained. In addition, equity markets tend to move in cycles which may cause stock prices to fall over short or extended periods of time. Other Fund risks include market risk, liquidity risk, large cap, mid cap, and small cap risk. Please see prospectus for details regarding risk.

Shares are bought and sold at market price (closing price) not NAV and are not individually redeemed from the Fund. Market price returns are based on the midpoint of the bid/ask spread at 4:00 pm Eastern Time (when NAV is normally determined), and do not represent the return you would receive if you traded at other times.

Holdings and allocations are subject to risks and to change.

The views in this commentary are those of the portfolio manager and may not reflect his views on the date this material is distributed or anytime thereafter. These views are intended to assist shareholders in understanding their investments and do not constitute investment advice.