SURE: 2nd Quarter 2026 Portfolio Review

Portfolio Review

The U.S. equity market staged a remarkable recovery in the second quarter of 2026. What began against a backdrop of geopolitical uncertainty, volatile energy prices and questions about the durability of the artificial-intelligence trade ended with a powerful risk-on advance. The S&P 500 Index gained 15.20% for the quarter, one of its strongest quarterly results since 2020. The AdvisorShares Insider Advantage ETF (SURE) gained 16.94% on a NAV basis, outperforming the S&P 500 by 174 basis points and the Russell 3000 Index by 150 basis points.

Technology and semiconductor shares led the rally from the March lows, supported by exceptionally strong demand for AI infrastructure. By quarter-end, however, participation had broadened beyond the largest growth companies. Equal-weight, small-cap and value benchmarks joined the advance as investors rotated across cyclicals, industrials, financials and health care. That broadening is important to SURE, which seeks company-specific opportunities rather than relying on a small group of mega-cap names to carry the portfolio.

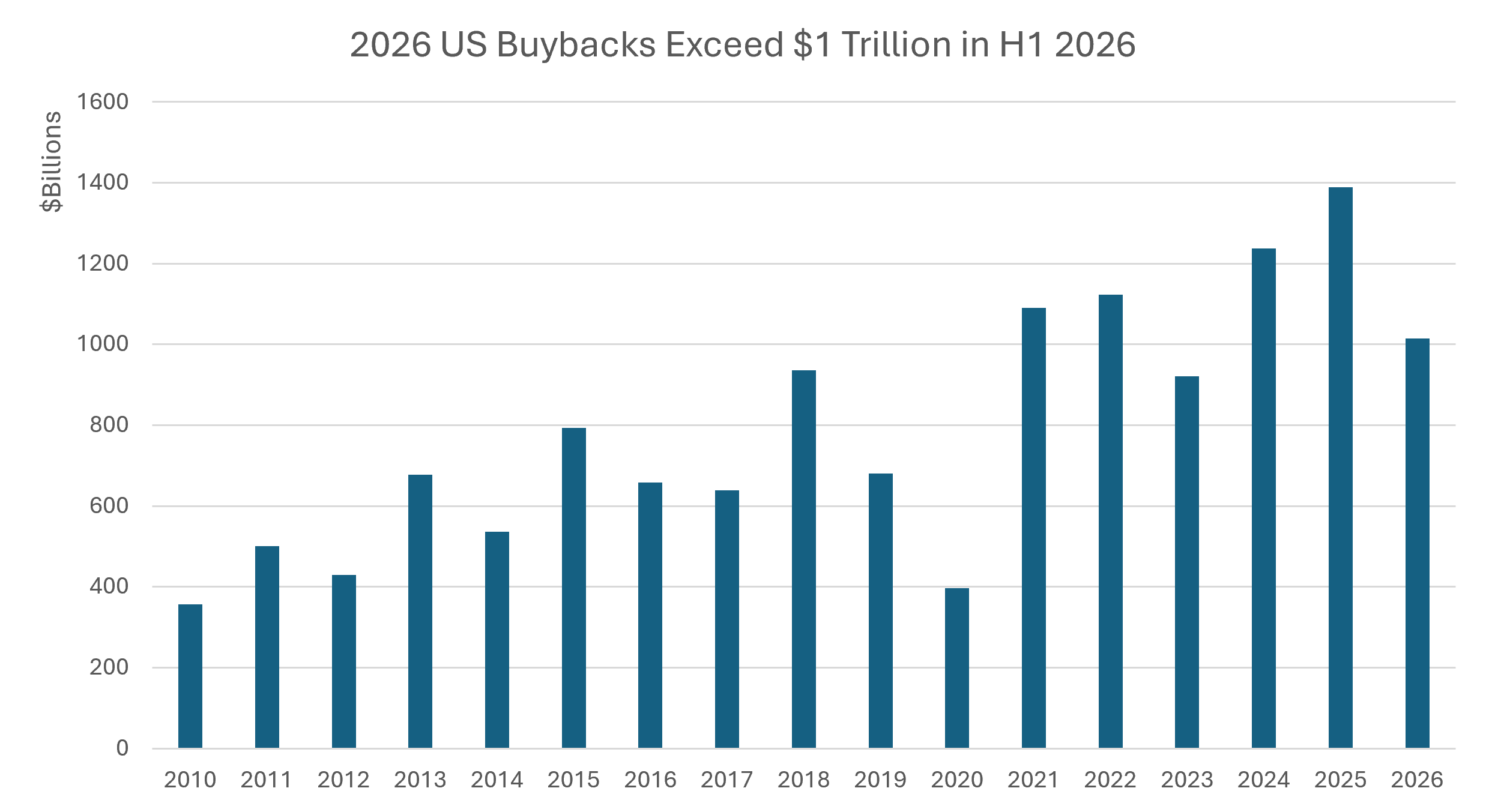

The corporate-buyback backdrop was equally striking. U.S. companies announced more than $568 billion of new stock buyback authorizations in the second quarter, another record high. New authorizations in the first half of 2026 already exceeded $1 trillion, up 33% from the $760 billion announced in the first half of 2025, a remarkable result given the market volatility of the past six months. The largest individual programs included Apple ($100 billion), Nvidia ($80 billion) and JPMorgan ($50 billion).

Source: Qubed Capital, 2026 data only include first six months.

For SURE, those headlines are a starting point rather than an endpoint. A well-executed repurchase program can reduce public float and signal management’s confidence in underlying cash flows, but not every authorization is equally compelling. Profitability, balance-sheet capacity and the price paid for shares all matter, particularly after a sharp market rebound. SURE’s process is designed to distinguish among those opportunities rather than simply follow headline buyback totals.

That discipline is applied through an actively managed, equal-weight process. SURE re-evaluates its investable universe and existing holdings monthly, returning each security toward an equal-weight allocation as it responds to changes in buyback programs, acquisitions and other company-specific developments. The underlying screen emphasizes shareholder-friendliness, free-cash-flow generation and balance-sheet strength. The fund holdings illustrate the result: SURE held 100 equity positions, no single holding exceeded 1.84% of portfolio assets, and the ten largest positions together represented approximately 15.6%.

The current portfolio also spans several distinct return drivers. Applied Materials, Lam Research and Marvell Technology illustrate the fund’s exposure to AI infrastructure, while energy holdings such as Chevron, Exxon Mobil and Marathon Petroleum add exposure to a different part of the economic cycle. Oil prices surged early in the period before retreating as geopolitical tensions eased and supply concerns moderated. This balance allows the fund to participate in powerful secular themes without requiring a single forecast on oil, rates or technology valuations.

As the market enters the second half of 2026, attention will turn from the strength of the rebound to the durability of earnings growth. Semiconductor demand and AI capital spending remain powerful forces, but investors will increasingly look for evidence that elevated expectations are being met. The late-quarter expansion in market participation suggests that opportunity may continue to broaden. In this environment, we believe SURE’s monthly, buyback-focused approach remains well positioned to seek attractive shareholder-return opportunities while managing the concentration risks that can emerge in cap-weighted benchmarks.

Top Holdings

| Ticker | Security Description | Portfolio Weight % |

| MRVL | MARVELL TECHNOLOGY INC | 2.09% |

| AMAT | APPLIED MATERIALS INC | 2.00% |

| SEZL | SEZZLE INC | 1.96% |

| LRCX | LAM RESEARCH CORP | 1.73% |

| DVA | DAVITA INC | 1.68% |

| FTNT | FORTINET INC | 1.63% |

| IRDM | IRIDIUM COMMUNICATIONS INC | 1.58% |

| KLAC | KLA CORP | 1.53% |

| CAT | CATERPILLAR INC | 1.40% |

| EVER | EVERQUOTE INC – CLASS A | 1.37% |

As of 06.30.2026. Holdings are subject to change.

Respectfully,

Respectfully,

Minyi Chen

Qubed Capital, LLC

AdvisorShares Insider Advantage ETF (SURE) Portfolio Strategist

Past Commentary

– A buyback (or repurchase) occurs when a company repurchases its own shares from the marketplace, reducing the number of shares outstanding. – An insider is an officer, director, executive, entity, or individual that owns more than 10% of a publicly traded company’s shares. – Insider buying is the legal purchase of shares in a firm by a corporate insider that is not based on non-public, material information and follows the U.S. Securities and Exchange Commission’s rules and reporting requirements. – The S&P 500 Index is a broad-based, unmanaged measurement of changes in stock market conditions based on the average of 500 widely held common stocks. One cannot invest directly in an index.

*On September 1, 2022, the AdvisorShares DoubleLine Value Equity ETF (the “Predecessor Fund”) was renamed the AdvisorShares Insider Advantage ETF. The Predecessor Fund had different portfolio managers and investment strategy than the AdvisorShares Insider Advantage ETF. Performance prior to September 1, 2022 reflects the Fund’s performance prior to the change in manager and investment strategy and may not be indicative of the Fund’s performance under the new manager and revised investment strategy. Performance since September 1, 2022 reflects actual AdvisorShares Insider Advantage ETF performance.

Before investing you should carefully consider the Fund’s investment objectives, risks, charges and expenses. This and other information is in the prospectus or summary prospectus, a copy of which may be obtained by visiting the Fund’s website at www.AdvisorShares.com. Please read the prospectus carefully before you invest. Foreside Fund Services, LLC, Distributor. The Fund’s investment focus follows a core philosophy that corporate insiders know their companies best. The Advisor believes that insider buying and stock buyback programs not only show that corporate insiders see relative value in investing in their own company’s equity securities, but also create favorable market conditions by reducing public equity float (i.e., the share supply available to investors on the public secondary market). The Advisor allocates the Fund’s portfolio using research from a disciplined and quantitative proprietary model, the U.S. Insiders Edge Model, developed by Qubed Capital, LLC. In utilizing the model, the Advisor seeks to remove emotion from day-to-day decision-making by following a systematic process. The Fund is an actively-managed exchange-traded fund (“ETF”) that seeks to achieve its investment objective by primarily investing in a portfolio of U.S. traded companies selected from a universe of the largest 3,000 U.S. equity securities based on market capitalization. When models and data prove to be incorrect or incomplete, any decisions made in reliance thereon expose the Fund to potential risks. In addition, the use of predictive models has inherent risk. The views in this commentary are those of the portfolio manager/strategist and may not reflect his views on the date this material is distributed or anytime thereafter. These views are intended to assist shareholders in understanding their investments and do not constitute investment advice.